French Budget Bill 2026

2026

-

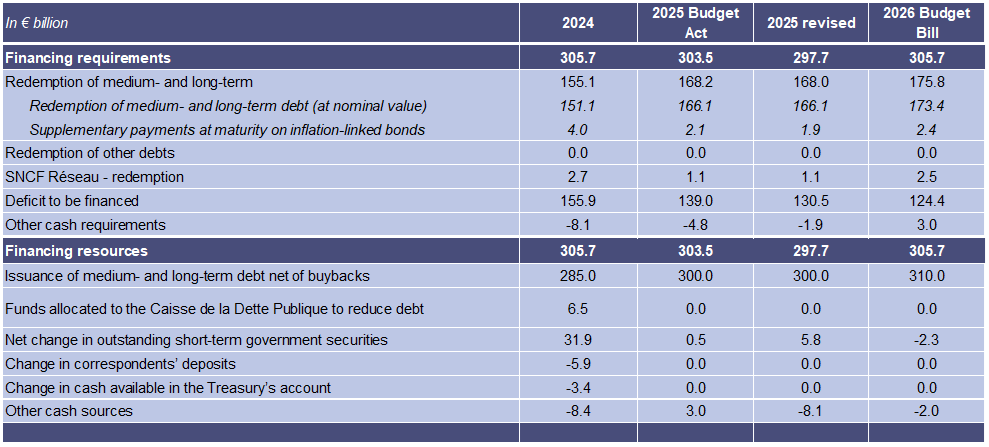

The French Budget Bill for 2026 was presented today to the Council of Ministers. The total financing requirement will stand at €305.7bn, marking a €8.0bn increase compared to the 2025 updated financing requirement. The increase in this requirement is mainly due to the depreciation of medium- and long-term securities, which increased by €7.8 billion (€175.8 billion in 2026 compared to €168.0 billion in 2025). The deficit shown in the State financing table for 2026 amounts to €124.4 billion (compared to €130.5 billion for 2025).

-

The financing requirement in 2026 will be met by the medium- and long-term government debt issuance programme, net of buybacks, worth €310bn. In addition, the outstanding short-term government securities (BTFs) will decrease by €2.3bn. Other cash resources amounted to -€2.0 billion.

-

State debt service is expected to stand at €59.3bn.

-

The net year-on-year increase in the nominal value of negotiable State debt with maturities of one year or more will be capped at €136.6bn.

-

The detailed medium- and long-term financing programme for 2026 will be released in December 2025

2025

-

For 2025, issuance of medium- and long-term debt, net of buybacks, remains unchanged at €300.0bn.

-

The deficit to be financed in 2025 has been revised downwards to €130.5bn, compared to the amount of €139.0bn provided for in the 2025 initial Budget Act promulgated in February 2025.

-

“Other cash resources” are projected at -€8.1bn, mainly as a result of discounts at issuance, compared to €3.0bn in the 2025 initial Budget Act.

-

Outstanding BTFs will increase by €5.8bn, against €0.5bn in the 2025 initial Budget Act.

-

Since the beginning of 2025, the weighted average yield of medium- and long-term debt securities issued stands at 3.16%, compared to 2.91% in 2024. The weighted average rate on BTF issues decreased significantly, falling to 2.14%, compared to 3.39% in 2024.

-

State debt service is revised to €52.0bn for 2025, versus €54.9bn in the 2025 initial Budget Act.